IRS Extends R&D Tax Credit Reporting Deadlines — What Innovation-Driven Companies Need to Know

The Internal Revenue Service (IRS) recently issued important updates affecting how businesses claim the Research & Development (R&D) Tax Credit, a valuable federal incentive for companies investing in innovation. These changes provide additional time and procedural clarity for taxpayers adapting to new reporting requirements and documentation standards — particularly around the revised Form 6765 and the expanded Section G business component reporting.

Section G Reporting Remains Optional Through 2025

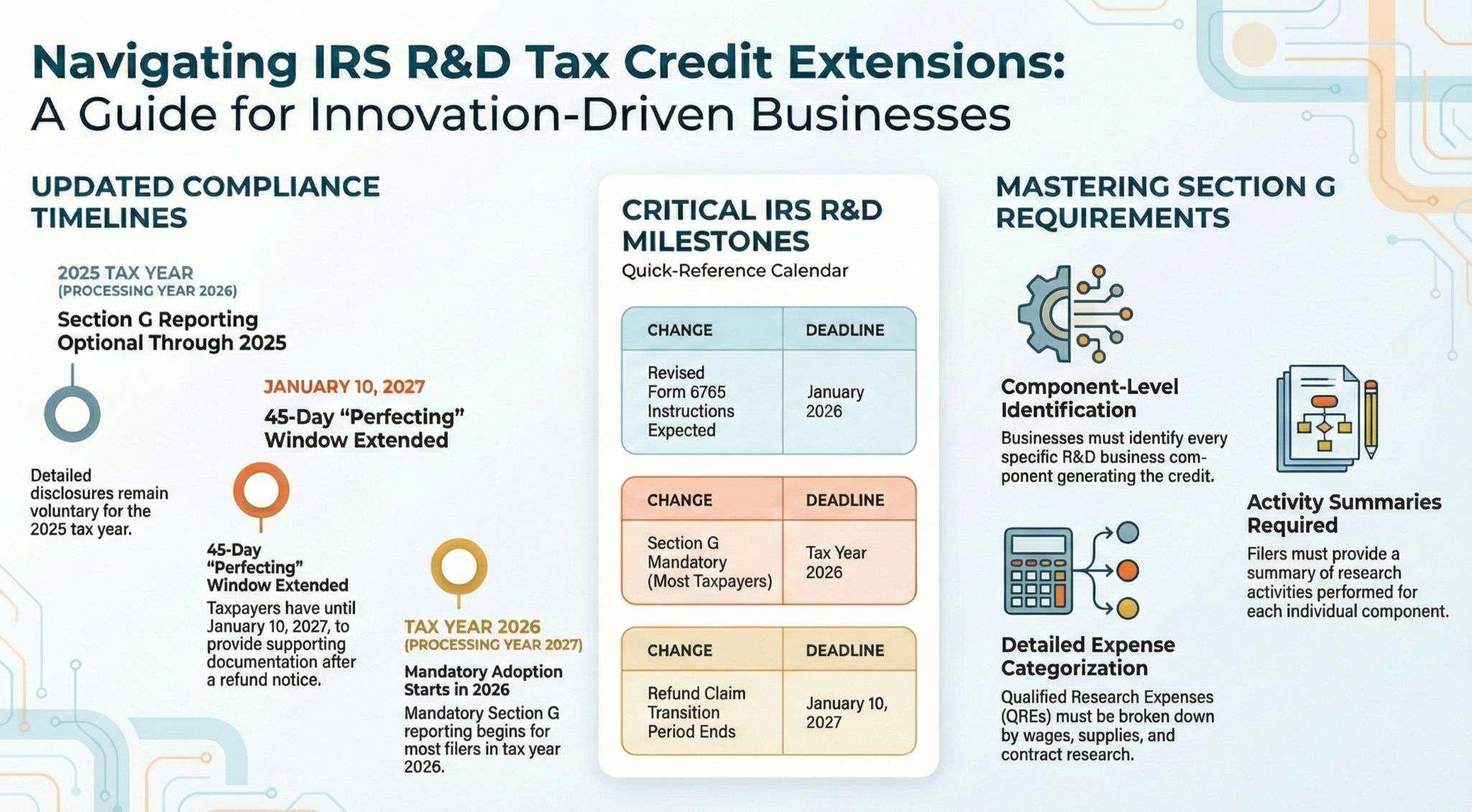

A major change announced in IRS news release IR-2025-99 (Oct. 1, 2025) confirms that Section G of Form 6765 — which requires detailed disclosures of research activities and qualified expenses by business component — will remain optional for all filers for the 2025 tax year (processing year 2026).

This extension reflects ongoing stakeholder feedback and gives businesses more time to prepare systems and documentation before mandatory reporting begins. The IRS also extended the comment period on the draft instructions for Form 6765 through March 31, 2026, and expects to release revised instructions in January 2026.

What Section G Requires (and Why It Matters)

Section G is designed to standardize how businesses report their R&D work and requires:

- Identification of R&D business components generating the credit

- A summary of research activities performed for each component

- A breakdown of Qualified Research Expenses (QREs) by category (e.g., wages, supplies, contract research)

Although optional for the 2025 filing season, Section G is expected to become mandatory for most taxpayers starting with tax year 2026 (processing year 2027), with limited exceptions for:

- Qualified small business (QSB) taxpayers electing the payroll tax credit, and

- Taxpayers with total QREs ≤ $1.5 million and gross receipts ≤ $50 million at the control group level, when claiming the credit on an original return.

Because Section G aligns with the types of detailed information IRS examiners already request during examinations and refund reviews, many tax advisors recommend preparing Section G information in advance, even while it’s optional.

Extended Transition Period for R&D Refund Claims

In addition to the Section G delay, the IRS also extended the transition period for R&D tax credit refund claims. Through January 10, 2027, taxpayers will continue to have 45 days after receiving an IRS notice to “perfect” a refund claim — meaning to provide supporting documentation — before the IRS makes a final determination.

For refund claims postmarked after June 18, 2024, the supporting documentation generally must include:

- Identification of all R&D business components associated with the claim

- Descriptions of research activities for those components

- Totals of qualified employee wage expenses, supplies, and contract research costs

This extension helps taxpayers avoid claim rejections based on procedural issues, but it does not lessen the substantive documentation expectations of the IRS.

What This Means for Innovation-Driven Businesses

The additional time provided by these IRS extensions is valuable — but it should be viewed as an opportunity to prepare rather than a reason to delay.

Key implications include:

- Section G formalizes increased project-level transparency that the IRS is increasingly expecting.

- The extended refund claim transition underscores the need for thoughtful, contemporaneous documentation.

Companies that proactively implement tracking systems capable of capturing:

- Activities tied to technical uncertainty,

- Project-level cost and role detail, and

- Clear, defensible narratives tied to the credit criteria

will be better positioned for both audit defense and the eventual mandatory adoption of Section G in 2026.

Key Deadlines to Remember

Change | Deadline |

Section G Optional Period | Through March 31, 2026 |

Revised Form 6765 Instructions Expected | January 2026 |

Section G Mandatory for Most Taxpayers | Tax Year 2026 (Processing Year 2027) |

Refund Claim Transition Extended | Through January 10, 2027 |

How Tributan Helps

At Tributan, we help innovation-driven companies navigate evolving R&D tax rules with a focus on rigorous documentation and defensible claims. Whether you’re optimizing current-year filings or building repeatable processes for future compliance, we support your team with:

- Mapping research activities to credit-qualified categories

- Structuring documentation that satisfies IRS expectations

- Preparing for Section G reporting and potential IRS review

If you’d like customized support, we’re here to help you innovate and comply with confidence.

Sources: IRS news release IR-2025-99; IRS.gov “IRS extends the period for feedback on Form 6765”; KBKG analysis of the extended transition period for Section G and refund claims.